The notice arrived on a Thursday. By Monday, state-licensed retailers across the country were scrambling to get re-underwritten with whichever processor had agreed to take the category next. The company I worked for had built its payment stack on debit-only workarounds (PIN-based card-not-present, stored-value, ACH) because the credit networks would not openly process the vertical. Legal. State-licensed. Regulated. And uninsurable, in the quiet sense of the word, because an executive at a bank somewhere up the chain had decided the arrangement had become too visible.

This happened every six to twelve months. Some retailers passed the re-underwriting. Some did not. Some lost a week of revenue. Some lost a month. A few closed, not because they had broken a law but because a private company with no mandate, no judicial review, and no appeals process had decided their legal business was too inconvenient to keep processing.

Then there was the big one. A coordinated exit. Every retailer in the network sent through underwriting at once, at the worst possible moment any business can have its payment infrastructure interrupted. That was the cycle I was sitting inside when the question that runs through this entire book finally had a shape I could state out loud.

Why can one private company decide commerce for another private company that is operating legally?

No one had elected the card networks. No one had appointed them. No statute had granted them the authority to declare a category off-limits. And yet they did. Routinely. At scale. Across borders. With no recourse that reached them.

That was the morning the abstraction became a specific thing I could point at.

The Same Beast, Twice

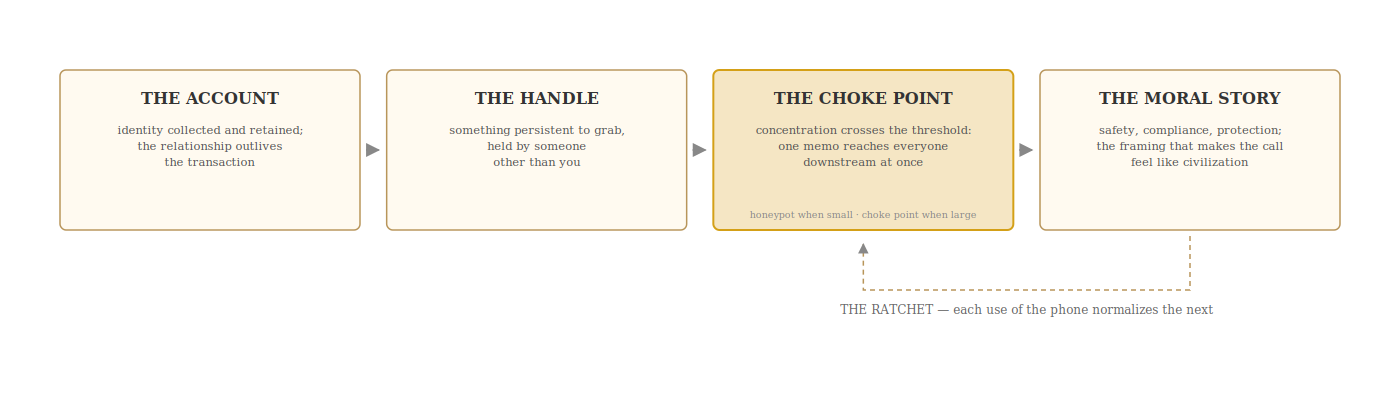

The same centralized system that is a honeypot when it is small becomes a choke point when it is large. Concentration of data invites breach. Concentration of flow invites pressure. The small system gets hacked. The large system gets called. Neither outcome is the result of anyone being clever or careless. Both are properties of what concentration does to anything placed inside it.

A payment rail begins its life as a database. Merchant IDs, customer records, transaction logs, card numbers, identity documents. Each field, alone, is a column. Together they are a target. A small rail serving ten thousand merchants is a honeypot no intelligent attacker needs to be briefed on. The return on a successful intrusion writes itself. The rail grows. The database grows. The compliance obligations grow, and the compliance obligations generate more data, which grows the database again. By the time the rail has a market share worth calling market share, it is a data set that governments subpoena, journalists request, and criminals pay brokers to exfiltrate.

Then the same rail crosses a threshold. Enough merchants depend on it that an interruption produces a political event. Enough consumers have saved their cards on it that withdrawing access is socially expensive. At that point the rail is no longer only a database. It is a piece of infrastructure that other people’s lives route through. And the phone rings.

A regulator with a theory about some category of commerce. A senator with a hearing coming up. A journalist with a column going to print tomorrow. A shareholder with a quarterly concern. Each of them has the same instrument available. Pressure applied to the choke point reaches everyone downstream of it at once. The rail does not have to agree with the caller. It only has to do a risk calculation about what happens if it does not.

The honeypot is the early failure mode. The choke point is the mature one. They are not two different problems. They are the same architecture growing up.

The Two Words

In the payments industry, a category of commerce is not banned. It is high risk.

The phrase sounds technical. It is not. High risk is not a mathematical statement about chargeback rates or fraud incidence. Genuinely high-chargeback categories like used cars, furniture, and airline tickets carry normal processing terms. High risk is a political and reputational classification. It names the categories a bank does not want on its books when the wrong person notices.

Once two words attach to a category, they do the work of permitting everything that follows. Higher processing fees, yes. That is the visible consequence. But also: arbitrary termination, no-notice holds on settled funds, mandatory personal guarantees from owners who already carry corporate liability, quarterly re-reviews, monthly disclosures, lifetime blacklists across the MATCH file that processors share with each other. Each of these would be contested in any other industry. In a high risk category none of them are contested, because the anchor has already done the work. If a merchant is high risk, everything done to them is proportional by definition. The word proves itself by the treatment it permits.

And the anchor is available to anyone who operates a rail. A merchant category can be moved onto the high-risk list by a policy update, a compliance memo, a reputational calculation inside a single risk committee. No new law is required, no judicial review, no public hearing. Two words, one afternoon, one memo. And a legal industry has been relocated one shelf up on the regulatory danger scale, where the terms are worse, the termination rights are easier, and the merchants are told to be grateful they have any processing at all.

The Public Versions

Most of the adult-entertainment story is public record.

In August 2021, OnlyFans told its creators that sexually explicit content would be banned. The CEO said it plainly. Banking partners and payment processors had demanded it. The decision was reversed a week later, but by then subscribers had canceled, creators had scattered, and the lesson was permanent. The platform had not made a content decision. A bank had.

In December 2020, Visa, Mastercard, and Discover cut off processing for Pornhub. After a single column by Nicholas Kristof in The New York Times. By 2021, every adult-content platform was required to pre-review all uploaded material, monitor streams in real time, and maintain identity records for every performer. By 2022, advertising revenue was blocked as well.

Between 2013 and 2017, the U.S. Department of Justice ran the same play against a whole shelf of high risk industries at once, in a program called Operation Choke Point; The Receipts documents it, dates and committee findings included. What belongs in this chapter is the part that outlived it. The program was officially ended; the capability it named was not. Banks still make the same risk calls, card networks still set the same content policies, processors still terminate the same categories. The program was never the mechanism. It only named what the mechanism was always able to do.

The adult industry is the public version of this story because somebody wrote about it. The mechanism is identical and the phone call is the same phone call; only the retailers change. The vertical next to mine was another public version, for anyone sitting close enough to watch.

The Privacy Inversion

The honeypot end of the same architecture has a human cost the choke point does not. For most industries a data breach is embarrassing. For some it is existential. People have been blackmailed with purchase histories from adult platforms; careers have ended because a name appeared in a database that should never have existed. The compliance apparatus designed to control the rail produces, as a byproduct, an ever-expanding attack surface for the people it claims to protect.

The industry’s response, imposed by the same payment networks that caused the problem, has been to require more data, not less: more ID verification, more records, more fields that become bigger targets. The people with the most to lose from exposure are forced to provide the most data. That is not a policy failure. It is the policy working as designed, for someone else’s definition of working.

The Phone Number

Every private payment rail is a company. Every company has a phone number. Anyone with enough leverage can pick it up.

The architecture of centralized payment processing is not merely vulnerable to this. It is an invitation. The phone exists. The pressure will come. The only variable is who calls and what they want shut down.

A public protocol has no phone. Bitcoin does not have a compliance department. Lightning does not have a risk committee. There is no one to call, no one to pressure, no one who wakes up Monday morning worried about brand risk. The protocol does not care because it cannot care. And the inability is the point.

This is not ideology. The adult industry adopted online payments before Amazon not out of any philosophical commitment to financial innovation but because the alternative was not getting paid. They will adopt the blind rail for the same reason. Every system with a phone number will eventually get the call. They have answered it enough times to know.

Unpopular Is Not a Jurisdictional Standard

The categories that get anchored high risk are the ones that happen to be unpopular, inconvenient, or undefended at the moment the decision is made. Today the list contains adult entertainment, firearms, cannabis in states where it is legal, payday lending, tobacco, vaping, online gambling, and supplements with contested health claims. Ten years ago the list contained some of these and not others. Ten years from now it will have changed again. The mechanism does not change. The targets do.

Journalists whose reporting embarrasses the wrong person. Political organizations whose fundraising moves a number the wrong direction. Religious groups whose theology falls out of fashion. Climate activists. Vaccine skeptics. Firearms collectors. Crowdfunding campaigns for causes the wrong foundation publicly opposes. Each of them has, at various points in the last decade, had their payment access disrupted or revoked, not by court order but by a compliance memo, a board decision, a reputational calculation.

Unpopularity is not a jurisdictional standard. It is a weathervane. Today it points at one group. Tomorrow it points at another.

If you are reading this and the current categories on the list happen not to include yours, that is a property of the current weather, not of the mechanism.

The financial system has a kill switch, and they found it first. A public protocol does not have one, because on the old rails the payment is the identity, the identity is the control layer, and the phone number was always the feature.